Bitcoin’s rebound to round $71,000 has reignited a well-recognized bullish conversation about worth, liquidity, and positioning. It has additionally uncovered a much less comfy reality contained in the community itself.

The charge market has barely moved.

For a market that also treats on-chain congestion as an indication of natural demand, that divergence deserves extra consideration than one other recap of macro tailwinds or ETF movement streaks.

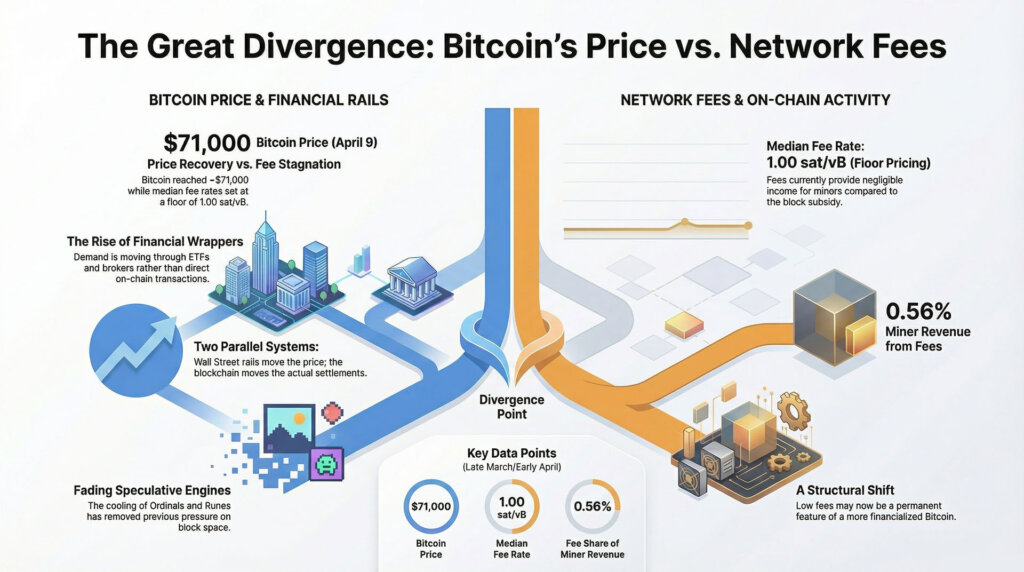

On CryptoSlate’s Bitcoin price page, BTC was final buying and selling at $70,990 on April 9, down 0.86% over 24 hours, up 6.11% over seven days, and up 0.85% over 30 days.

Worth has clearly recovered from the decrease finish of its current vary, whereas the bottom layer nonetheless appears calm, low-cost, and uncrowded.

The disconnect says one thing essential about the place this transfer is definitely occurring. Extra Bitcoin demand is being expressed by means of monetary wrappers, dealer channels, and ETF rails than by means of customers competing for block area on-chain.

The value transfer can nonetheless be sturdy beneath that setup. The sign it sends is totally different.

A current Bitcoin block space report overlaying March 19 to March 26 discovered that the median charge fee opened at 1.13 sat/vB and remained at 1.00 sat/vB for the remainder of the week. In sensible phrases, that’s flooring pricing.

Customers have been nonetheless in a position to get confirmed with out paying up for scarce area. Throughout 1,028 blocks, the report counted simply 18.03 BTC in complete charges, or roughly 0.0175 BTC per block.

Much more putting, these charges accounted for less than 0.56% of miner income for the week, in contrast with 3,212.5 BTC from subsidy.

Worth has recovered, whereas the charge market nonetheless appears half asleep

These numbers are unusually mushy for a market buying and selling again round $71,000. Earlier cycle logic conditioned the market to count on a rising Bitcoin worth to coincide with busier blocks, extra contested inclusion, and a charge market that begins climbing earlier than most individuals discover.

That reflex nonetheless shapes what number of crypto contributors interpret demand. The present market is sending a distinct message.

Worth can get well even whereas on-chain urgency stays muted.

One motive the charge market appears so subdued is that Bitcoin has already misplaced one of many speculative demand engines that distorted block-space pricing in prior phases. Ordinals and different inscriptions as soon as created a visual burst of non-monetary demand for inclusion, whereas the Runes launch briefly did the identical on a fair bigger scale across the 2024 halving.

That impulse has pale materially. The chain is not coping with the identical inscription-driven scramble for block area, which implies at this time’s low-fee surroundings isn’t just a narrative about wholesome effectivity or quiet consumer habits.

It additionally displays the absence of a class that had beforehand inflated transaction counts and put strain on charges.

That context helps clarify why a rebound in BTC can coexist with such a mushy charge backdrop. Earlier within the cycle, Ordinals, inscriptions, and later Runes gave miners an additional income stream and gave observers a motive to deal with mempool stress as proof of increasing demand.

Right now, that help appears a lot thinner. The speculative site visitors that after crowded the chain has cooled, leaving Bitcoin extra depending on both natural settlement demand or price-led monetary flows to do the heavy lifting.

In that sense, it is also about what has already left the constructing.

A part of that dynamic comes from the truth that the pipes carrying demand have modified. A purchaser utilizing a spot ETF, a dealer product, or a treasury car can push capital into Bitcoin publicity with out creating the identical base-layer footprint as a consumer transferring cash immediately throughout the chain.

That distinction has grown extra essential as Bitcoin entry has turn into extra financialized. Farside’s daily ETF flow data confirmed a $471.4 million influx on April 6, adopted by outflows of $159.1 million on April 7 and $124.5 million on April 8.

The day-to-day swings have been comparatively modest, but the broader level is that flows by means of these wrappers stay an energetic transmission channel for demand. Spot Bitcoin ETFs recorded $1.3 billion in internet inflows for the month, the primary optimistic month since October.

That’s the hidden mechanism behind the present divergence. Bitcoin demand is being break up throughout two programs.

One system strikes worth by means of funds, adviser platforms, and dealer entry. The opposite system strikes transactions by means of the blockchain itself.

Proper now, the primary system appears extra energetic than the second. That leaves the charge market trying sleepy even because the asset itself regains altitude.

The result’s a rebound that feels bullish on screens, whereas the community’s personal pricing of block area stays subdued. That mixture carries a distinct implication than a full-on-chain revival.

It suggests the restoration has broad distribution by means of monetary rails, whereas direct strain on Bitcoin’s settlement layer stays restricted. For anybody nonetheless treating mempool stress as a easy proxy for demand, the present setup is a reminder that the market construction round Bitcoin has modified sooner than lots of the instincts individuals nonetheless use to interpret it.

Glassnode’s April 1 weekly market note described Bitcoin as rangebound between $60,000 and $70,000 and argued that spot demand was exhibiting early indicators of absorption, whereas nonetheless missing the conviction wanted for a sustained breakout. Glassnode additionally flagged dense overhead provide between $80,000 and $126,000.

That vary framework matches the present divergence nicely. Bitcoin has bounced, but the charge market has not repriced to point broad urgency, widespread settlement demand, or a sudden scramble for base-layer entry.

Low charges level to the place demand is touchdown, and to what miners nonetheless will not be getting paid for

A separate report citing Glassnode information on March charge exercise stated Bitcoin’s 30-day easy transferring common for every day transaction charges had fallen to 2.5 BTC per day in March 2026. The article described that because the lowest stage since March 2011.

The exact historic framing requires warning till the underlying major chart is checked immediately, but the directional message strains up with the broader proof. Payment circumstances have tightened considerably, they usually have stayed tight whilst BTC regained floor.

That compression creates an essential divide between worth energy and community monetization. Customers get a friendlier chain. Miners get little or no incremental income from transaction demand.

After the halving, that income combine carries extra weight than it did when the subsidy was doing much more of the work. The March 19 to March 26 block area report quantified the difficulty cleanly, with charges contributing simply 0.56% of miner income for the week.

For miners, a rally that doesn’t set off a charge response nonetheless helps by means of worth, whereas leaving the community’s inside income base largely unchanged.

The distinction turns into simpler to see as soon as Bitcoin is framed as each an asset and a community, with both sides expressing demand in numerous methods. The asset facet advantages from ETF adoption, adviser entry, treasury accumulation, and improved danger urge for food.

The community facet advantages from precise customers, transfers, settlements, and transactions that compete for restricted capability. These two layers can reinforce one another.

They will additionally drift aside for significant stretches. That’s the place the market sits now.

There may be additionally a sensible level within the present setup. A peaceful mempool doesn’t mechanically translate into weak Bitcoin.

It means that the rebound affords much less proof of resurgent on-chain depth than the worth alone may indicate. A base-layer charge response would point out that monetary demand was spilling over into precise settlement competition.

With out that response, a distinct interpretation strikes nearer to the middle: one wherein Wall Avenue distribution is doing extra of the rapid lifting than customers transacting natively on-chain.

That outside-world collision offers the present divergence its explanatory energy. Bitcoin is more and more embedded in mainstream monetary plumbing.

Morgan Stanley has simply launched a low-fee spot Bitcoin ETF, and Charles Schwab is making ready direct spot Bitcoin and Ethereum buying and selling by mid-2026. The entry channels round Bitcoin proceed to widen.

As they widen, worth can transfer alongside these rails lengthy earlier than the mempool alerts an analogous demand pulse.

The following check sits within the charge market, the miner income combine, and whether or not worth energy spreads into precise settlement demand

The rapid query is whether or not the present divergence is momentary or structural. There are credible arguments on either side, and the subsequent few weeks ought to assist slender the vary of believable outcomes.

The primary path is a continuation of the present sample. ETF and dealer demand proceed to help the worth; Bitcoin holds close to the higher finish of its current vary, and charge charges stay near the ground.

That might strengthen the case that this rebound is being carried primarily by wrapper-led flows slightly than a broad-based return of native transaction demand. It might additionally reinforce the concept that worth can get well by means of distribution and entry to capital, whereas the chain’s personal charge market stays calm.

The second path is a catch-up transfer in block-space demand. If the worth restoration begins to spill over into precise transaction competitors, the market ought to begin to see larger charge estimates, deeper backlogs, extra sustained strain within the mempool, and a bigger charge share in miner income.

That shift would change the interpretation of the rally. It might recommend that the transfer is spreading from publicity into utilization, which might give the restoration a distinct sort of sturdiness.

The third path would go away the present divergence trying extra like a warning than a curiosity. If ETF flows roll over once more, worth slips again into the decrease half of Glassnode’s current vary, and charge circumstances nonetheless keep weak, the market can have stronger grounds to deal with the rebound as a positioning transfer that by no means developed into broader transactional demand.

In that setup, the mempool’s quietness would cease trying incidental and begin trying diagnostic.

A fourth path sits nearer to miner economics than worth course. If charges stay this subdued whereas miners proceed working in a post-halving surroundings, consideration will shift towards how the community is being monetized.

CoinShares’ Q1 2026 mining report described the ultimate quarter of 2025 because the hardest quarter for miners for the reason that 2024 halving, with a pointy worth drawdown and near-record hashrate weighing on margins. A protracted stretch of low charges would preserve that strain in focus.

Worth appreciation helps, whereas a broader charge contribution would assist extra.

That’s the reason the charge market deserves to take a seat a lot nearer to the middle of the present Bitcoin dialog. A transfer again towards $71,000 is significant.

It additionally leaves an open query. The place, precisely, is the demand changing into actual?

Proper now, the strongest reply is that demand is changing into actual in monetary merchandise sooner than it’s in Bitcoin’s personal block area.

That carries a measured however essential implication for the way this market ought to be understood. The rebound has gained traction by means of the channels Bitcoin spent years making an attempt to enter: funds, advisers, brokers, and mainstream portfolio plumbing.

The blockchain itself has but to point out the identical urgency in its pricing of entry. For anybody watching Bitcoin as each a financial asset and a community, that hole is the sign.

The market has moved larger. The chain has barely flinched.

The following spherical of proof will come from whether or not that calm lastly breaks, or whether or not Bitcoin’s strongest demand engine now lives one layer faraway from Bitcoin itself.