Bitcoin’s on-chain image is flashing a uncommon mixture: substantial income throughout cohorts, rising realized capitalization, and report community hashrate—but not one of the price-accelerating euphoria that usually marks late-stage bull legs. That’s the central takeaway from CryptoQuant CEO Ki Younger Ju’s newest thread, which parses holder price bases, cohort profitability, leverage, and the evolving position of ETFs and company treasuries in setting the tape.

Is The Bitcoin Bull Run Over?

The headline quantity is startling on its face. “Bitcoin wallets’ avg price foundation is $55.9K, that means holders are up ~93% on common,” Ju wrote, including that realized capitalization climbed by roughly $8 billion this week, a clear learn that “on-chain inflows stay robust.” Realized cap—an alternate valuation measure that sums cash at their final transacted value quite than as we speak’s market value—has traditionally served as a lower-variance proxy for true money-at-work. Its continued rise usually implies that recent price foundation is being set greater on chain, even when spot stalls.

So why hasn’t value budged in tandem? Ju’s reply is easy: “Value hasn’t gone up due to promoting stress, not as a result of demand was weak.” That framing is in keeping with a market digesting features whereas liquidity suppliers and worthwhile cohorts distribute into power. It additionally helps clarify the co-existence of wholesome inflows with flat value motion across the $110,000 deal with that Ju cites as the present print.

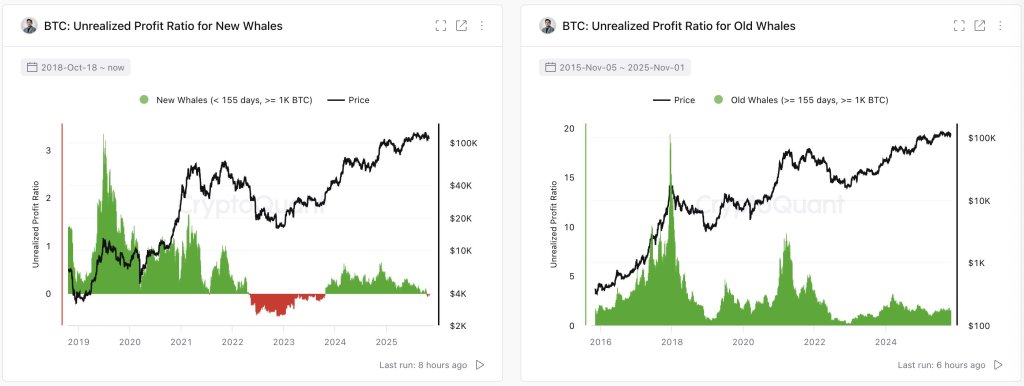

The place the marginal demand is coming from—and the place it has slowed—issues. In response to Ju, “New inflows largely come from ETFs and Bitcoin treasury firms, whereas CEX merchants & miners are sitting on ~2x features.” He broke out estimated cohort price bases and mark-to-market efficiency as follows: “ETFs / Custodial Wallets: $112K (-1%), Binance Merchants: $56K (+96%), Miners: $56K (+96%), Lengthy-term Whales: $43K (+155%). Present Value: $110K.”

If these estimates maintain, short-horizon institutional patrons are hovering close to breakeven, whereas long-tenured entities nonetheless carry deep embedded income. That distribution dampens compelled promoting danger on the very high but additionally withholds the type of recent momentum that usually arrives when new patrons push decisively into the cash.

Valuation context helps. Ju notes that in pronounced bull phases, market cap tends to outrun realized cap, making a widening “valuation multiplier.” “When the expansion fee hole between market cap and realized cap widens, it exhibits a stronger valuation multiplier,” he wrote.

“Roughly $1T in onchain inflows has created a $2T market cap. The hole appears reasonable for now.” A reasonable hole is a double-edged sign: not clearly frothy, but additionally not the type of exuberant enlargement that ends cycles. It enhances Ju’s evaluation of large-holder positioning: “Whales’ unrealized income aren’t excessive.” That state of affairs admits two interpretations he spelled out explicitly: “Hype hasn’t arrived but—we’re nonetheless removed from euphoric sentiment.” Or, “This time is totally different—the market is simply too huge for excessive revenue ratios.”

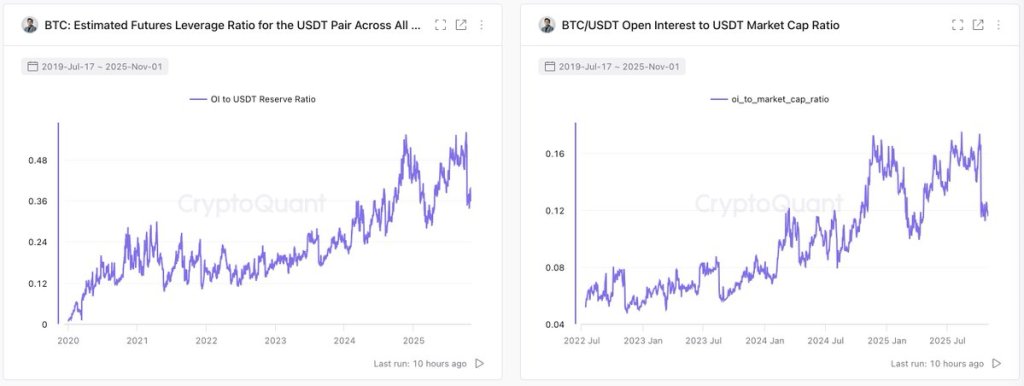

Perpetuals and collateral flows spherical out the microstructure image. Ju highlights a “sharp” drop in BTC shifting from spot-focused venues to futures exchanges—a sign that “whales are now not opening new lengthy positions with BTC collateral as actively as earlier than.”

If the marginal lengthy is now not pledging cash, the market loses a mechanical supply of bid depth and convexity from collateralized positioning. But leverage itself has not reset: “Bitcoin perp leverage stays excessive regardless of the recent wipeout,” Ju writes, pointing to ratios corresponding to BTC-USDT perpetual open curiosity relative to change USDT balances and to USDT market cap.

In easy phrases, conviction longs seem much less collateral-heavy in BTC, however system-wide leverage, as proxied by perps, stays elevated versus two years in the past. That mixture can suppress clear trending habits: fewer collateralized longs to chase upside, however sufficient leverage within the system to impose uneven liquidations.

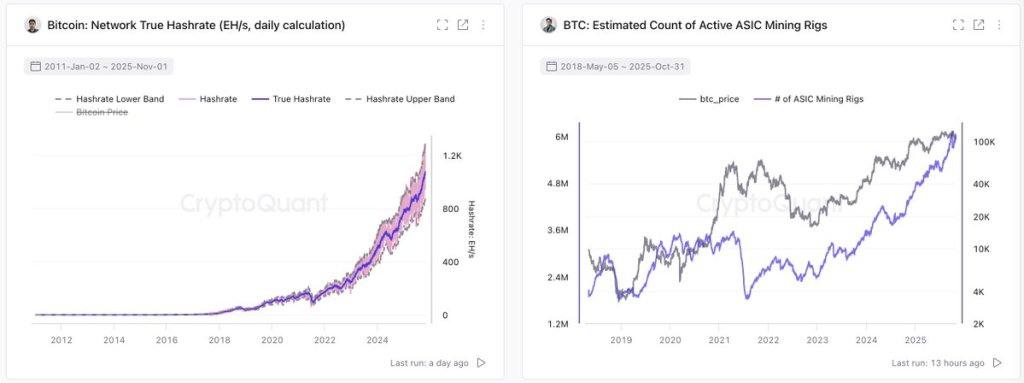

Hashrate and industrial provide traits complicate the narrative additional. “Bitcoin hashrate retains hitting new highs (~5.96M ASICs on-line). Public miners are increasing, not downsizing, which is a transparent long-term bullish sign. The Bitcoin ‘cash vessel’ retains rising.”

Rising hashrate plus increasing public miner fleets usually factors to ahead funding and confidence in long-run charge and subsidy economics. It doesn’t, nonetheless, assure short-term value appreciation; if something, it could possibly increase miner treasury administration wants, interacting with market liquidity in methods which are neutral-to-price absent recent demand.

New Demand Push Wanted

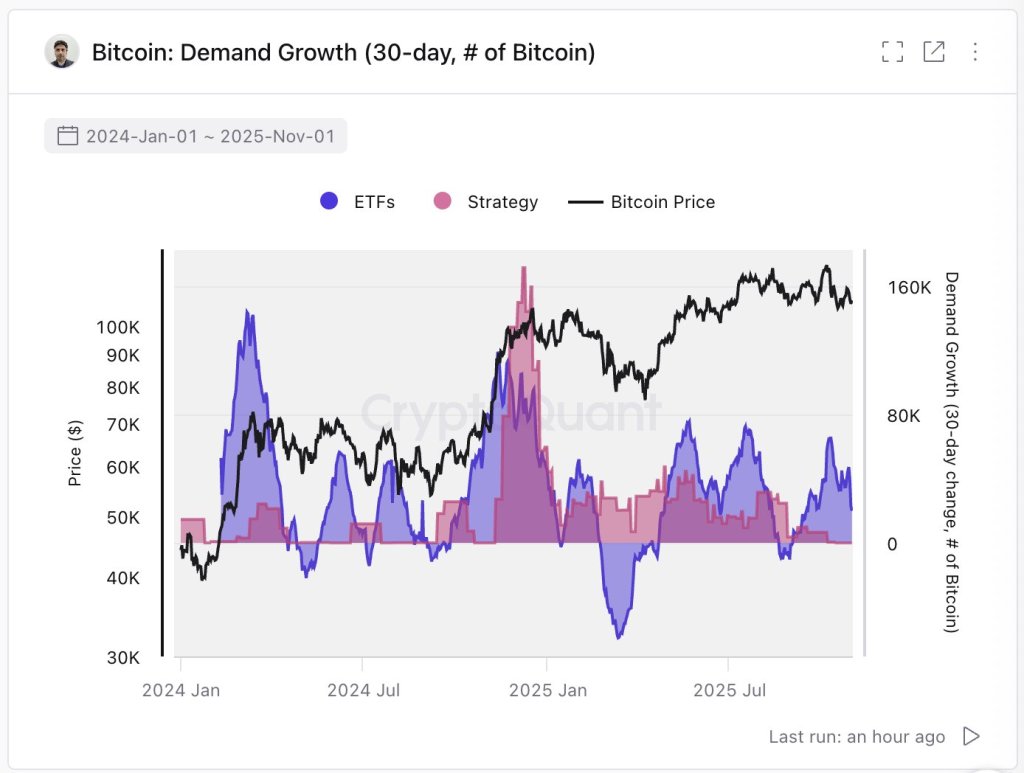

The demand facet, in Ju’s learn, is presently dominated by two channels: “Demand is now pushed largely by ETFs and Strategy, each slowing buys lately. If these two channels get better, market momentum seemingly returns.” That may be a clear, falsifiable thesis: if main institutional conduits re-accelerate, spot ought to regain buoyancy; if they continue to be tepid, realized cap can nonetheless grind greater on regular inflows whereas value chops as distribution absorbs them.

Cohort profitability supplies a further boundary situation for situations. “Brief-term whales (mostly ETFs) from the previous 6 months are close to break-even. Lengthy-term whales are up ~53%,” Ju wrote. Traditionally, cycle tops have typically coincided with excessive unrealized revenue ratios for dominant cohorts, creating structural promote stress when each marginal uptick unlocks vital features.

Ju is successfully saying we aren’t there. On the identical time, he cautions that the market’s regime could have already decoupled from the textbook four-year cadence: “Prior to now, the market moved in a transparent four-year cycle of accumulation and distribution between retail traders and whales. Now it’s tougher to foretell the place and the way a lot new liquidity will enter, making it unlikely for Bitcoin to comply with the identical cyclical sample once more.”

Taken collectively, the thread sketches a market with three defining traits. First, fundamentals of “cash in” look resilient: realized cap rising, holders broadly in revenue, and community safety hitting new highs. Second, microstructure is unspectacular and even a contact cautionary: fewer whales seeding BTC-collateralized longs, whereas system leverage stays excessive sufficient to destabilize clear strikes. Third, the demand baton is concentrated in ETF and company treasury channels which have lately eased off—the very actors whose re-acceleration might reignite momentum.

At press time, BTC traded at $107,609.

Featured picture created with DALL.E, chart from TradingView.com